The most recent Canaan monetary outcomes additionally reveal new divisions amongst Bitcoin mining’s most outstanding {hardware} suppliers. The corporate, which sells mining machines, reported a considerably weaker quarter simply as its crypto holdings grew to become inconceivable to disregard.

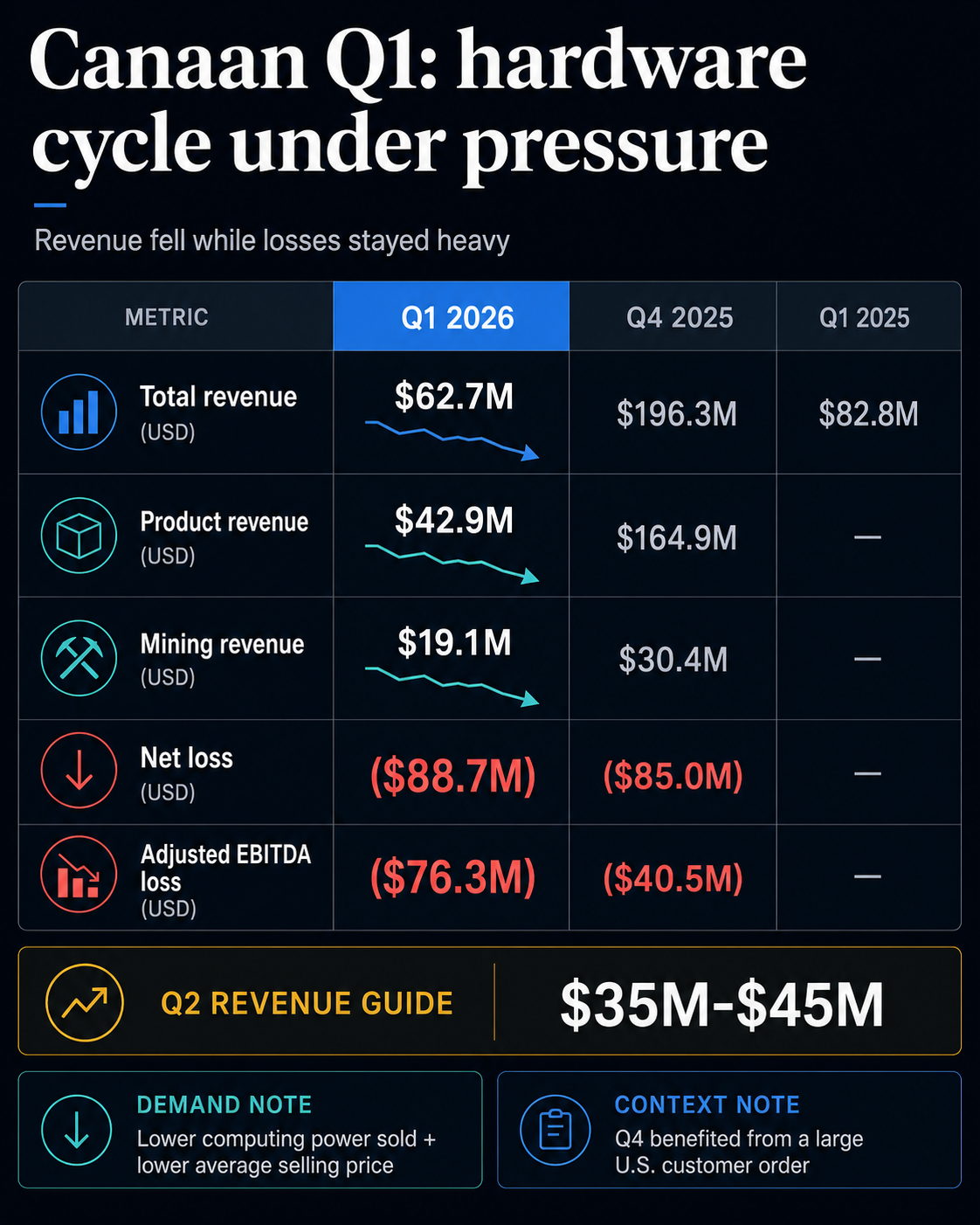

The ASIC maker introduced income for the primary quarter of 2026 fell to $62.7 million, down from $196.3 million within the earlier quarter and $82.8 million within the year-ago interval.

Web loss widened to $88.7 million from $85 million within the fourth quarter, and non-GAAP adjusted EBITDA loss practically doubled from $40.5 million to $76.3 million.

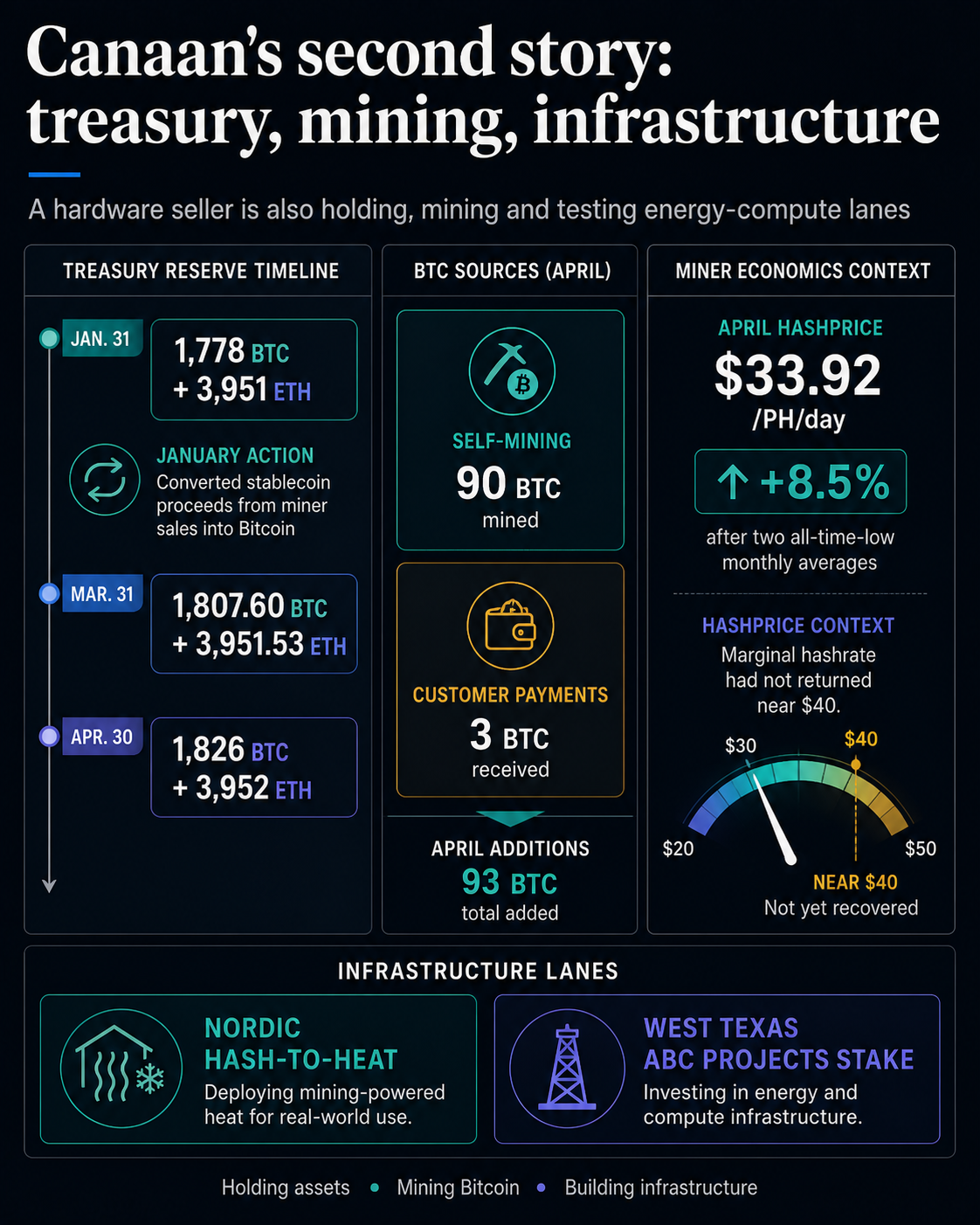

On the similar time, Canaan ended March with 1,807.60 BTC and three,951.53 ETH, setting new information for the corporate’s crypto treasury.

in crypto slate With value ranges of roughly $77,200 per BTC and $2,100 per ETH on Could 22, the stack was value roughly $148 million on a spot market foundation earlier than accounting, bond, or liquidity constraints.

That is the stress throughout the quarter. Canaan nonetheless sells machines that energy Bitcoin mining, however wanting on the reported numbers, it more and more seems like an organization with a weakening {hardware} cycle on the one hand and a rising stability sheet associated to BTC on the opposite. This decline additionally displays sluggish demand for Bitcoin mining as a result of tight miner financial system.

| metric | Q1 2026 | context |

|---|---|---|

| complete income | $62.7 million | Down from $196.3 million in This fall 2025 |

| product income | $42.9 million | Down from $164.9 million in This fall 2025 |

| mining income | $19.1 million | Down from $30.4 million in This fall 2025 |

| internet loss | $88.7 million | Greater than $85 million in This fall 2025 |

| crypto treasury | 1,807.60 BTC and three,951.53 ETH | Report excessive stage as of March 31, 2026 |

| Q2 earnings information | $35 million to $45 million | decrease than first quarter income |

The necessary level is the {hardware} cycle.

Canaan’s product segments reveal why {hardware} income, minor economics, and monetary publicity ought to all be learn collectively. ASIC miner income decreased to $42.9 million from $164.9 million within the fourth quarter of 2025.

The corporate mentioned this decline displays decrease computing energy offered and decrease common promoting costs, which is expounded to tighter market demand following the Bitcoin value drop.

This illustration is necessary as a result of ASIC producers are positioned on the higher reaches of the minor financial system. If miners are assured that they’ll recoup their prices on new machines, {hardware} orders can carry ahead income.

Demand for brand new {hardware} can shortly weaken as revenue margins are compressed by energy prices, difficulties, financing, or hash value pressures.

There was additionally some company-specific noise in Canaan’s Q1 comparability. The fourth quarter benefited from massive orders from U.S. prospects, after which the decline was even steeper.

Nonetheless, the demand language within the first quarter launch nonetheless factors to broader points. The {hardware} line displays each weaker unit demand and decrease common costs.

Outdoors Canaan, the miners’ financial scenario was nonetheless recovering from troublesome circumstances. In response to the April 2026 lookback of the Hash Charge Index, the typical hash value in USD rose 8.5% to $33.92 per PH per day after the month-to-month common hit new all-time lows twice.

Regardless of hash costs returning to close $40 in early Could, marginal hashrate has not returned to the community, the corporate mentioned.

bookmydollar’s personal mining protection tracks the identical pressures from a unique angle. Earlier this yr, miners had been in no hurry to carry their machines again on-line even after the worth rebounded, emphasizing that spot Bitcoin alone doesn’t decide whether or not a rig can be worthwhile.

Energy costs, issue, machine effectivity, and stability sheet liquidity are all necessary.

For Canaan, it turns the product’s income line right into a key sign. The corporate has two associated exposures: Bitcoin value fluctuations and miners’ willingness to justify new capital funding in machines.

The primary quarter instructed that demand was not but robust sufficient to soak up the working base of {hardware} sellers.

Treasury is a counterweight

The opposite facet of the story is that Kanan’s Bitcoin treasury and ETH holdings continued to develop.

In its mining replace for January, the corporate introduced that it transformed stablecoin proceeds from miner gross sales into Bitcoin, with reserves reaching 1,778 BTC and three,951 ETH on the finish of the month.

By March thirty first, Q1 outcomes confirmed 1,807.60 BTC and three,951.53 ETH. On the finish of the quarter, Canaan introduced that its April operations added 90 BTC from self-mining and three BTC from buyer funds, bringing the stability to 1,826 BTC and three,952 ETH by April thirtieth.

This mechanism adjustments the way in which you take a look at the quarter. Canaan’s crypto asset balances presently replicate ongoing operational selections in parallel with its conventional holdings.

A portion of miners’ gross sales income has been transferred to Bitcoin, and self-mining continues so as to add BTC despite the fact that mining income has declined since This fall.

The excellence is necessary. Pure ASIC suppliers rely on buyer demand for his or her machines. Miners rely on operational effectivity, energy prices, hash costs, and Bitcoin manufacturing.

Treasury holders are dependent in the marketplace worth of the property they maintain. Kanan now has all three components, making it troublesome to interpret reported weaknesses by a single lens.

Working losses stay a counterpoint. The corporate reported a internet lack of $88.7 million within the first quarter, and gross sales within the second quarter had been solely $35 million to $45 million, decrease than the already weak first quarter outcomes.

This steering means the stability sheet might be an enormous a part of the story, for the reason that revenue assertion has but to point out any indicators of restoration.

Canaan’s spot estimate of BTC and ETH of roughly $148 million additionally must be restrained. This helps with scale, however the market worth is completely different from Canaan’s accounting worth, and investor motivations are nonetheless unproven.

With out proof of market capitalization and inventory costs, a extra correct argument is that Treasury is now of sufficient substance to belong close to the highest of the story.

Infrastructure offers Canaan a 3rd lane.

Canaan’s Q1 launch additionally promoted a broader infrastructure message. The corporate highlighted its hash-to-heat enlargement in Northern Europe and its funding within the West Texas ABC venture, which is positioned nearer to power and computing infrastructure than conventional equipment gross sales.

These particulars lie behind the core numbers, however they assist clarify why Canaan is wanting past the following ASIC order cycle.

As mining margins tighten, public miners are already gravitating towards power, internet hosting, AI or high-performance computing methods. bookmydollar has coated how public miners are leveraging Treasury and infrastructure pivots to navigate the post-halving market.

Canaan variations are completely different as a result of they’re upstream. The corporate sells to miners, operates its personal mining publicity, owns a rising crypto stack, and checks energy-related infrastructure tasks.

The mix might assist the corporate if {hardware} demand stays weak, however it additionally makes the funding story extra difficult. Patrons of Canaan inventory are studying on ASIC gross sales, Bitcoin value publicity, self-mining manufacturing, and administration’s capacity to show infrastructure tasks into lasting returns.

This complexity is what retains this quarter from being a narrative of fundamental deviations and expectations. Canaan’s prospects are underneath stress, product income has considerably decreased, and on the similar time its personal crypto balances have grow to be extra noticeable.

Sellers of mining machines at the moment are uncovered to the property that their machines are constructed to provide.

The following take a look at is straightforward. The query is whether or not Q2 earnings and product costs stabilize sufficient that Q1 seems like a weak transition quarter, or whether or not Canaan-induced decline pushes the story additional into treasury, self-mining, and infrastructure exposures.

Even when buyer demand improves, Canaan is more likely to be primarily a cyclical ASIC provider with growing BTC and ETH balances. If revenues decline in step with steering and the crypto stack continues to rise, the market may have extra motive to deal with the corporate as a hybrid of {hardware} vendor, miner, Bitcoin treasury, and power calculation operator.

Thus far, the supply information bear out tensions fairly than clear verdicts. The primary quarter confirmed a slowdown within the {hardware} enterprise, widening losses, a decline in mining income, and a rise in crypto property.

This mix makes Canaan one of many clearest examples of how Bitcoin mining transactions are altering. Even firms that promote picks and shovels are more and more taking up asset dangers that their prospects face each day.

The corporate remains to be closely uncovered to demand for Bitcoin mining {hardware} regardless of its elevated monetary publicity. The broader query after these Canaan features is whether or not Treasury progress can offset weak {hardware} demand.