Technique, the Bitcoin monetary and enterprise software program firm previously referred to as MicroStrategy, has spent years turning the general public markets right into a funding engine for Bitcoin purchases. This mannequin has helped make the corporate the world’s largest company holder of digital belongings.

At present, the securities used to drive that technique are beneath stress.

The strain is centered on STRC, Technique Inc.’s floating-rate Sequence A perpetual stretch most well-liked inventory, a major financing automobile designed to commerce close to its acknowledged worth of $100.

As an alternative, STRC fell to an all-time low of practically $71 on Friday earlier than recovering to about $75, about 25% beneath par, elevating questions on whether or not the corporate will be capable of proceed elevating capital on favorable phrases.

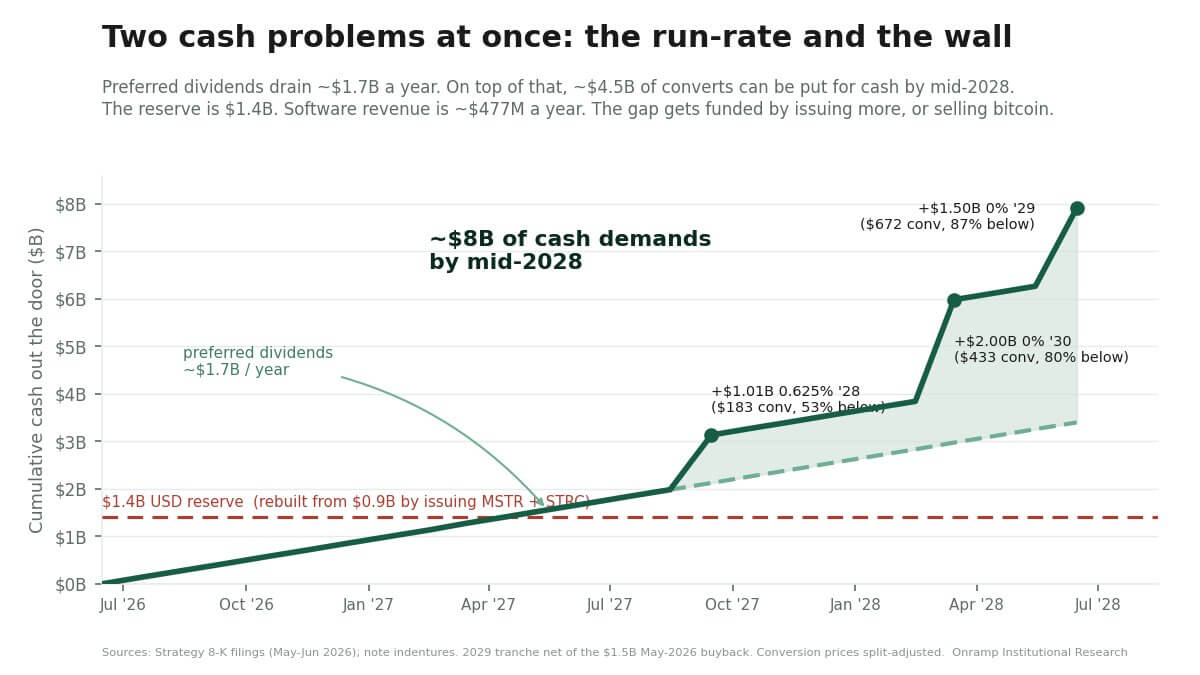

The decline comes as some market individuals face an $8 billion funding barrier and technique over the following two years, together with most well-liked dividend debt and convertible debt that shareholders can return to the corporate as money earlier than ultimate maturity.

This burden shifted buyers’ consideration from the scale of Technique’s Bitcoin holdings to the stability sheet constructed round it.

Technique loses Bitcoin premium

The shift turned evident on Friday, when Technique’s enterprise market-to-net asset worth fell beneath 1, quickly erasing the premium that had lengthy separated the corporate from different company Bitcoin holders.

This metric is necessary as a result of it seems past the spot worth of Bitcoin in Technique. It incorporates the corporate’s debt, money, and most well-liked inventory, giving a whole image of how your entire construction Saylor has constructed round its belongings is valued within the public market.

Subsequently, whether it is beneath parity, this means that buyers will not be paying further for Technique’s capacity to build up Bitcoin by means of public market lending. As an alternative, they low cost the complexity and price of claims sitting within the firm’s treasury.

This marks a reversal from the offers that outlined Technique’s rise. For years, the corporate was in a position to promote shares and different securities at excessive valuations and use the proceeds to purchase extra Bitcoin.

This premium created a robust loop during which greater market worth helped fund extra purchases, and extra purchases strengthened the corporate’s place as a number one publicly traded Bitcoin company.

However when frequent and most well-liked shares fall on the similar time, it turns into tough to remain in the identical loop.

The truth is, Technique’s frequent inventory fell to a two-year low of $82 on Friday. In the meantime, Bitcoin was additionally struggling beneath $60,000.

Bitcoin traits are now not the one concern for shareholders. The query is whether or not Technique can proceed to entry the capital markets with out deepening dilution, rising money prices or placing strain on its inventory holdings.

Technique faces $8 billion funds check

In the meantime, the technique debate is more and more shifting away from Bitcoin alone and towards the less complicated query of how a lot money corporations will want if market circumstances stay hostile.

Glenn Cameron, international head of establishments at Orrump Bitcoin, estimates that Technique may face round $8 billion in potential money wants over the following two years.

He mentioned the strain is coming from two locations. One is a most well-liked inventory stack that can be used to finance the Bitcoin buy, and the opposite is a convertible notice which will need to be paid again in money if frequent inventory costs proceed to say no.

Most popular shares already generate massive run charges. Prime Minister Cameron pegged Technique’s annual most well-liked dividend legal responsibility at practically $1.7 billion, with STRC alone accounting for about $1.2 billion. This estimate is predicated on roughly 104.9 million STRC shares and an annualized rate of interest of 11.5% on the acknowledged worth of $100 of most well-liked inventory.

As STRC trades additional beneath par, that distortion will increase. Most popular inventory is structured with a variable dividend charge that goals to carry the safety nearer to its acknowledged value of $100.

Nevertheless, greater rates of interest additionally enhance the price of holding the product engaging to buyers, particularly if the market calls for greater yields to carry junior technique publicity.

At about $75, STRC’s efficient yield has risen to about 15%, indicating that buyers are on the lookout for a lot greater compensation than the acknowledged dividend charge signifies.

This doesn’t imply that Technique is going through a direct liquidity occasion, however it does point out that the popular lender has moved from an affordable funding device to a dearer a part of the capital construction.

The second strain level is convertible debt. Prime Minister Cameron has recognized round $4.5 billion value of notes that holders may probably return to the Technique as money between September 2027 and June 2028.

Potential reimbursement dates embody roughly $1.01 billion on September 15, 2027, roughly $2 billion on March 1, 2028, and roughly $1.5 billion on June 1, 2028.

These notes turn into extra vital if Technique’s frequent inventory trades effectively beneath its conversion value. If the inventory stays underfunded, holders have much less cause to transform to inventory and extra cause to hunt reimbursement in money if circumstances allow.

That is how the funding barrier approaches the $8 billion determine. Most popular dividends are carried out behind the scenes, mixed with convertible bonds which will require intensive money.

Technique holds roughly $1.4 billion in money to satisfy this potential demand. The corporate rebuilt a few of that buffer after drawing it down earlier, however it did so by promoting securities in a weak market. This helped keep liquidity, but additionally elevated the chance of additional dilution.

Subsequently, corporations’ decisions have gotten more and more constrained. Attainable choices embody promoting frequent inventory, issuing most well-liked inventory, refinancing debt, delaying Bitcoin purchases, or promoting a few of your Bitcoin holdings.

Nevertheless, none of those choices are freed from price.

Issuing frequent inventory dilutes the worth of present holders. Because the variety of most well-liked shares will increase, the dividend burden will increase. When technique securities are beneath strain, refinancing depends upon investor urge for food.

On the similar time, a delay in Bitcoin purchases would weaken the buildup story that has outlined the corporate. Promoting Bitcoin could be essentially the most radical departure from a method constructed round indefinite accumulation.

STRC trades like “junk credit score” as bears goal $60

Whereas STRC’s decline has been in comparison with previous crypto failures, the stress in Technique’s most well-liked inventory is going on by means of a special mechanism.

Blockchain intelligence agency Arkham Intelligence disagrees with the comparability between STRC and Terra’s LUNA, arguing that Strategic most well-liked inventory doesn’t perform like an algorithmic stablecoin. There is no such thing as a automated peg protection mechanism, and falling beneath the $100 threshold won’t itself set off a liquidation occasion.

This distinction is necessary as a result of STRC is a perpetual most well-liked safety and never a redeemable token. It’s beneath Technique’s debt in its capital stack, has no set maturity date, and doesn’t require the corporate to repurchase it at par on a set schedule. Dividends are cumulative, however money funds are topic to board approval and the corporate’s capacity to boost capital.

These options make Technique extra versatile than cryptocurrency buildings constructed round compelled redemptions and collateral liquidations. It additionally explains why STRC can commerce effectively beneath par with out inflicting a direct mechanical collapse.

The market is sounding one other warning. STRC is now not valued as a safety that naturally reverts to its acknowledged quantity of $100. Buyers are treating this like a yield-bearing declare to the technique’s capacity to proceed paying dividends, protect money, and lift capital whereas Bitcoin stays beneath strain.

This has introduced STRC nearer to expressions that emphasize company credit score somewhat than cryptocurrency-native leverage. Most popular inventory, priced roughly 25% beneath par, displays the next required return for buyers who tackle publicity to one of many firm’s junior debt obligations.

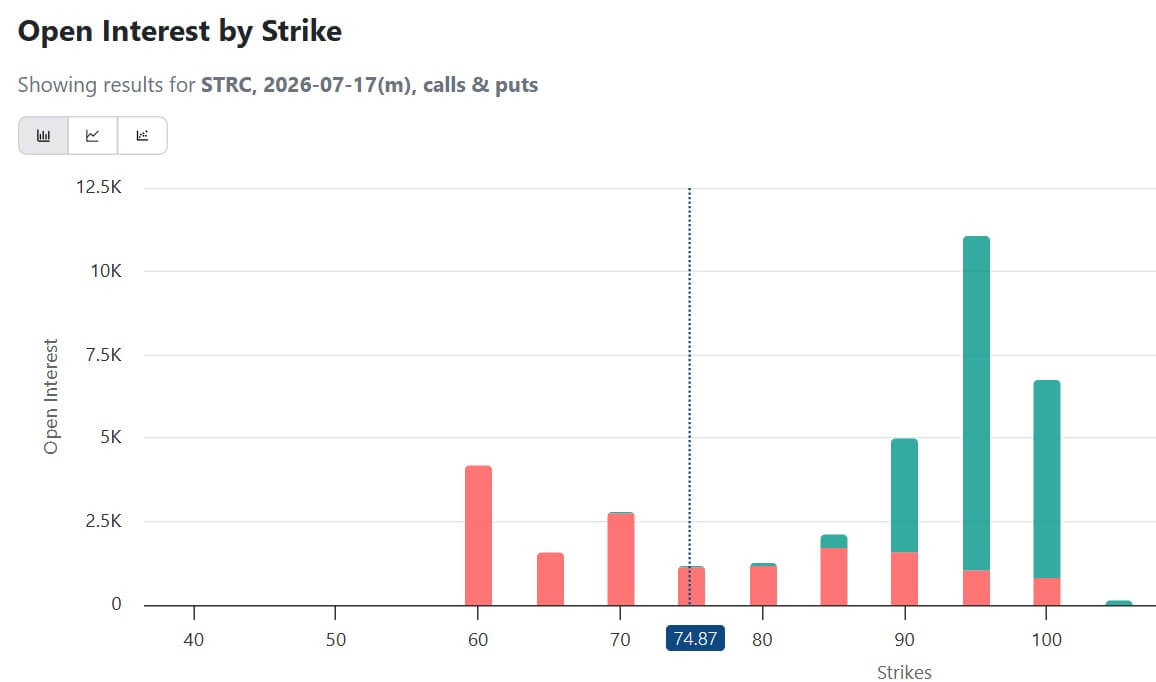

Notably, that strain is now exhibiting up within the choices market as effectively. Merchants have been constructing bearish positions round STRC, with excellent open curiosity on the July 17 contract with a strike value of $60.

This positioning means that some buyers are bracing for additional declines if confidence in most well-liked shares continues to say no.

Technique’s Bitcoin mannequin comes beneath criticism

The tensions throughout Technique’s securities have uncovered the corporate to harsher criticism from throughout the digital asset trade.

Ripple CEO Brad Garlinghouse mentioned Saylor’s fundraising technique in an interview with CNBC on Friday, arguing that the corporate’s reliance on most well-liked inventory and different capital market instruments is diverting consideration from what in the end brings worth to digital belongings.

In accordance with him:

“Monetary engineering doesn’t drive long-term worth. The long-term worth of digital belongings can be pushed by utility.”

Whereas Garlinghouse stays bullish on Bitcoin, he pointed to the decline in STRC as proof that the technique’s mannequin is beneath strain. He added:

“Michael Saylor on the group wasn’t centered on the precise issues, and that damage your entire market.”

These feedback spotlight the widening philosophical divide in cryptocurrencies. Saylor’s strategy is constructed round Bitcoin’s shortage, public market entry, and repeated accumulation. Garlinghouse’s critique displays a utility-first perspective on digital belongings, with an emphasis on funds, settlements, and tokenized monetary infrastructure.

That disagreement has been occurring for years. However what has modified is that the market is giving critics new proof.

So long as Bitcoin rose and Technique’s securities traded at a premium, the corporate’s mannequin gave the impression to be self-reinforcing. It may promote securities and purchase extra Bitcoin, probably capitalizing on investor enthusiasm to fund the following spherical of accumulation. The identical construction now seems extra susceptible as a result of decrease STRC, decrease MSTR, and smaller company mNAV.

Nevertheless, Michael Saylor dismissed these considerations, saying:

“Volatility checks any capital construction. Our technique stays centered on Bitcoin, disciplined capital allocation, credit score high quality, and long-term worth creation.”

The subsequent check can be whether or not the technique can restore confidence with out weakening what has made it some of the necessary Bitcoin brokers within the public markets.