JPMorgan views Wall Avenue’s transfer to non-public blockchains as a extra critical risk to Bitcoin than Methods promoting BTC.

JPMorgan warned that transferring tokenization, funds, and settlement to closed networks may drain exercise, liquidity, and capital from cryptocurrencies, resulting in decrease valuations.

A hybrid public-private system, stricter stablecoin guidelines, and Bitcoin’s endurance as digital gold may nonetheless upset that outlook.

Swift mentioned 17 banks throughout six continents, together with Citi, HSBC, Normal Chartered, UBS, Wells Fargo and Itau Unibanco, will start stay testing tokenized deposit funds on the brand new blockchain ledger, opening the door to 24-hour cash transfers.

On Could 4, DTCC introduced that greater than 50 firms, together with BlackRock, Goldman Sachs, Morgan Stanley, Nasdaq, and the New York Inventory Trade, have joined the tokenization working group, with plans to start restricted manufacturing buying and selling in July 2026 and full-scale launch in October.

How JP Morgan’s lawsuit stands

DTC already has over $114 trillion in property beneath custody, and DTCC subsidiaries processed $4.7 trillion in securities transactions in 2025.

When tokenized deposits are settled inside bank-managed ledgers and tokenized securities reside inside DTC’s personal infrastructure, their volumes by no means contact the charge markets, liquidity swimming pools, or token demand that Ethereum, Solana, stablecoin issuers, and RWA platforms depend on.

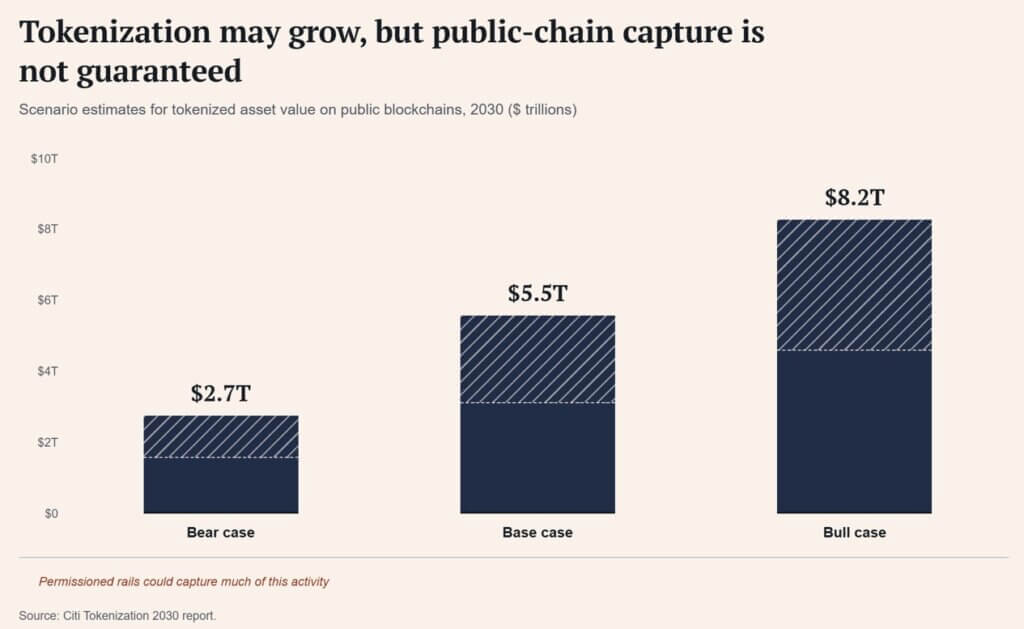

In accordance with Citi’s Tokenization 2030 Report launched in June 2026, the base-case tokenized asset market will attain $5.5 trillion by 2030, with a bear case of $2.7 trillion and a bull case of $8.2 trillion.

In its June 2026 annual report, BIS identified how that development will look, noting that whereas personal permissioned networks can meet the regulatory and governance wants of monetary establishments, in addition they danger creating walled gardens that stifle competitors and innovation.

What Wall Avenue desires from Bitcoin

BlackRock’s Spot Bitcoin ETF (IBIT) web page describes the product as offering publicity to the value of Bitcoin by an exchange-traded mechanism that eliminates the custodial and operational work concerned in proudly owning the asset straight.

IBIT had roughly $45.6 billion in internet property as of July 8, a determine that held regardless of a year-to-date NAV return of -28.93%.

Traders continued to park tens of billions of {dollars} in funds which have misplaced almost 30% of their worth this yr, a sample that resembles allocators securing shortage by essentially the most manageable wrapper.

Walled gardens are simple to know when you identify them. Financial institution-run ledgers can freeze balances, permissioned chains can exclude wallets, tokenized deposits nonetheless reply to the issuing financial institution, and a switch agent’s file can outweigh the tokens sitting on it.

Bitcoin is gradual, costly to maneuver at scale, and constructed for functions aside from regulated securities settlement, offering a ledger that’s outdoors the management of any single establishment and exists alongside sensible limitations.

This makes Bitcoin an asset outdoors of the system that Swift, DTCC, and a rising checklist of World Banks are constructing on.

| Options | Non-public financial institution ledger/tokenized deposits | Bitcoin |

|---|---|---|

| core performance | Speed up institutional funds, settlements, and asset recording | Uncommon bearer property outdoors the financial institution’s management |

| entry mannequin | Permits, KYC gates, institutional intermediaries | open community entry |

| management level | Financial institution, custodian, switch agent or market infrastructure supplier | Not a single establishment operator |

| Reversible/Freezable | Your stability or entry could also be frozen or restricted | Remittances usually are not managed by one establishment |

| Most important advantages | Compliance, velocity, liquidity effectivity and regulatory suitability | Neutrality, shortage and resistance to censorship |

| Most important weaknesses | Walled backyard, exclusion danger, restricted openness | Volatility, scaling limits, storage/safety dangers |

| JP Morgan’s dangers are most relevant to: | Public chain exercise, charges, liquidity, and token worth acquisition | Bitcoin provided that buyers deal with it as a basic cryptocurrency beta |

Bitcoin third throw

Bitcoin started as peer-to-peer digital money, however grew to become digital gold when ETFs included it of their allocations.

The period of personal chains provides us a 3rd paradigm: scarce property out there to everybody each time the digital rails cross a financial institution, custodian, or compliance gate.

The Fed saved its goal vary at 3.50-3.75% at its June 2026 assembly, and the greenback index was hovering round 100.93 as of July 9, amid geopolitical tensions and inflation issues.

Stablecoins nonetheless have the biggest public chain funds footprint, with DeFiLlama exhibiting round $311.9 billion in comparison with the almost $14.9 billion stablecoin market capitalization of tokenized U.S. Treasuries, which is just a fraction of the roughly $30 trillion U.S. Treasury market itself.

The above case is a story argument and there are actual limits to what may be assured relative to cost. JPMorgan Non-public Financial institution famous that Bitcoin’s volatility has been about 4 occasions that of worldwide equities over the previous decade, and famous {that a} 5% Bitcoin allocation elevated portfolio danger by 13%, in comparison with a 2% enhance for a comparable gold place.

Cryptocurrency firms are already bracing for the dangers posed by quantum computing, with some estimates suggesting that a good portion of Bitcoin’s provide may finally be uncovered if cryptography shouldn’t be upgraded.

On the bullish path, tokenization will develop in direction of the upper reaches of the Metropolis, with entry remaining gated, reversible, and bank-mediated each step of the best way. Public chain tokens lose the premium on the cost layer that JPMorgan’s argument targets, and spotlight Bitcoin’s traits of being uncommon, impartial, and never issued by any establishment.

The introduction of a personal chain will start to function a free commercial for one ledger unbiased of all of the banks that construct this method.

On the bear aspect, ETF outflows and risk-off markets dominate the narrative, with buyers studying the introduction of personal chains as proof that banks now management the infrastructure cryptocurrencies they as soon as promised to switch.

| situation | what should occur | What it means for public chain cryptocurrencies | What it means for Bitcoin |

|---|---|---|---|

| Bull path: walled backyard will increase the worth of the exit | Tokenization expands in direction of Citi cap, however entry stays gated, reversible, and bank-mediated | Public chain tokens will lose a number of the cost layer premium focused by JPMorgan | Bitcoin’s distinction strengthens as a uncommon, impartial forex outdoors of bank-controlled ledgers |

| Bearish path: banks win the infrastructure story | ETF outflows, risk-off markets and weak liquidity dominate sentiment | Non-public chain adoption interpreted as proof that banks have captured the promise of cryptocurrencies’ native infrastructure | Bitcoin trades in crypto beta regardless of its clear monetary concept |

| base path: each arguments coexist | Whereas banks tokenize funds, Bitcoin stays primarily an allocation asset within the ETF period | Exercise strikes to permitted rails, limiting some earnings on the general public chain | Bitcoin advantages narratively, however worth nonetheless is dependent upon flows, macro liquidity, and danger urge for food |

Bitcoin has fallen relative to different sectors as a result of its worth follows the sector’s total danger urge for food quite than its underlying narrative, regardless of how clear the speculation is.

In relation to Bitcoin, JPMorgan’s warning describes the asset’s oldest debate in actual time. A monetary system that solely a handful of establishments can program creates a singular demand for an asset that no different establishment can.