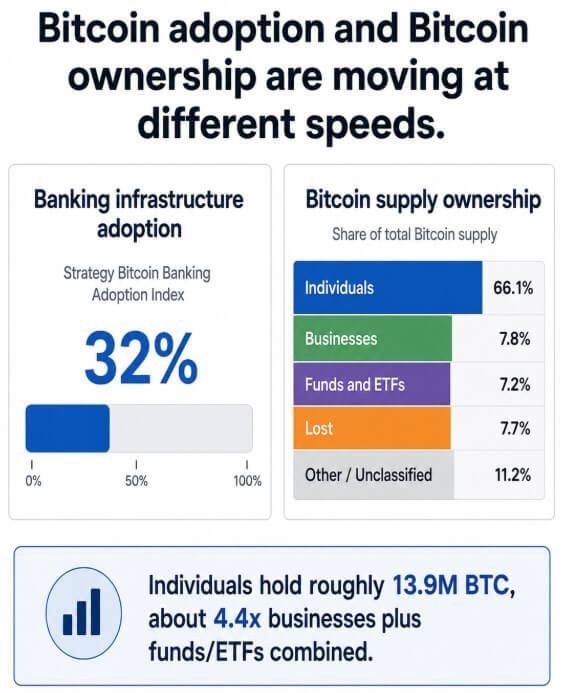

Technique’s new Bitcoin Financial institution Adoption Index provides 25 largest banks and monetary establishments an general rating of 32% based mostly on exercise throughout custody, buying and selling, funding merchandise, lending, and management assist.

This quantity is a depth rating that measures how effectively banks are constructing Bitcoin-related companies throughout establishments tracked by the technique.

Bitwise’s Q3 2026 Crypto Market Assessment estimates that 66.1% of Bitcoin’s most provide of 21 million (equal to roughly 13.9 million BTC) is held by people, dwarfing the 7.8% held by companies and the 7.2% held by funds and ETFs.

The final two classes and corporations, in addition to funds and ETFs, collectively account for less than about 15% of the provision, or about 3.15 million BTC price. Which means that people maintain almost 4.4 instances as a lot Bitcoin as each teams mixed.

People first established the possession base

Technique’s index tracks the extent to which banks have constructed plumbing round Bitcoin, scoring establishments throughout their custodial methods, buying and selling desks that execute orders, funding merchandise, lending packages, and public statements that exhibit an establishment’s consolation with the asset.

Banks that rating extremely on this index have constructed the infrastructure to retailer, commerce, lend, and package deal Bitcoin for his or her clients. Possession of the coin itself is exterior the scope of what the rating makes an attempt to measure.

The facility of retail is right here within the numbers, and it is why banks are increasing within the first place.

Banks are responding to a mixture of buyer demand, ETF progress, company treasury exercise, regulatory modifications, and competitors from crypto-native corporations.

Prospects already personal and use Bitcoin on a scale that banks can’t ignore, and this 32% rating displays banks responding to demand created by people years earlier than banks arrange custodial desks.

A big possession base permits banks to have an current pool of homeowners with which to compete with out having to create a market from scratch.

So the following contest will look totally different than most institutional adoption tales. Lengthy earlier than banks compete for cash that people may promote, they first compete with exchanges, specialised custodians, and account self-custody instruments that people are already utilizing.

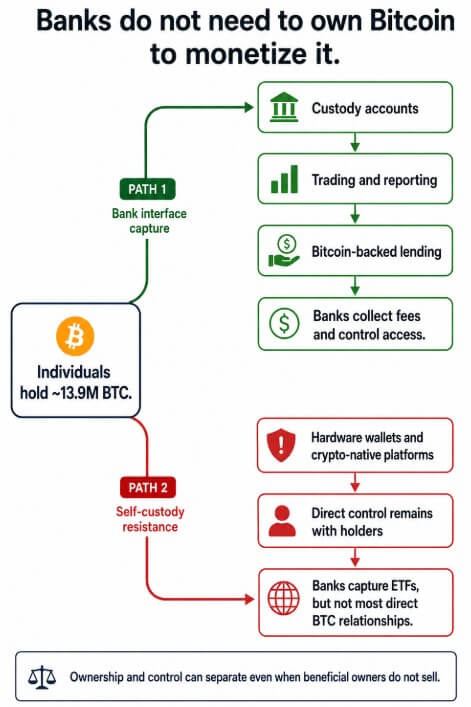

Possession and management have gotten separated

Banks can retailer their clients’ Bitcoin, execute transactions, handle collateral, and cost charges for these companies whereas the client stays the beneficiary. A buyer’s actual rights will fluctuate relying on the custody, brokerage, or mortgage settlement, together with the switch or rehypothecation of belongings.

This separates management of the client interface from authorized possession of the asset. As extra holders use brokered accounts, banks might have extra affect over entry, reporting and collateral phrases, however this index doesn’t show that banks have already got a bonus over exchanges or self-custody suppliers.

To place this into perspective, if 10% of the 13.9 million BTC belonging to a person have been transferred to a bank-managed custodial or securities account, roughly 1.39 million BTC would stay on the financial institution’s infrastructure. The remaining 90% will stay exterior of those accounts, whether or not underneath self-management or held with different intermediaries.

At 25%, roughly 3.47 million BTC could be positioned on bank-controlled rails. At 50%, this quantity could be nearer to six.94 million BTC. In every situation, the client’s possession and withdrawal rights rely on the custody, brokerage, or lending settlement.

| Instance of a private BTC share transferring to bank-managed rails | Affected BTC | What the financial institution advantages from | What a person holds |

|---|---|---|---|

| 10% | ~1.39 million BTC | Custody charges, commerce execution, reporting visibility, account relationships | Efficient possession of most cash |

| twenty 5% | ~3.47 million BTC | A serious foothold in Bitcoin storage, intermediation, and lending infrastructure | Possession, however much less direct management if held via an middleman |

| 50% | ~6.94 million BTC | Performs a central function in Bitcoin storage and buyer entry, and has potential affect on the collateral market | Possession of helpful pursuits is topic to custody circumstances, however entry and enforcement of the account is transferred to the financial institution. |

what occurs from right here

The SEC’s SAB 122 rescinded SAB 121, which directed entities defending the crypto belongings of platform customers to acknowledge liabilities and corresponding belongings on their steadiness sheets. The modifications take away accounting therapy that trade individuals cited as a barrier to providing crypto custody at scale.

The Fed has lifted the requirement for state member banks to offer advance discover earlier than starting crypto-asset actions and integrated its oversight into its common supervision.

The OCC stated banks can purchase and promote saved crypto belongings on the path of their clients as a part of their permissible custody companies. The Basel Committee Disclosure Framework on Banks’ Publicity to Cryptoassets will enter into pressure inside the Basel Framework on January 1, 2026 and requires qualitative and quantitative disclosures by internationally lively banks in member jurisdictions implementing the usual.

One doable path might be for Bitcoin-backed loans to develop into a extra widespread asset administration product, permitting banks to earn charges on collateralized loans with out proudly owning the underlying Bitcoin.

Whereas holders can borrow in opposition to Bitcoin whereas sustaining worth publicity, crypto-native lenders may face margin strain if banks provide decrease rates of interest or broader account consolidation.

Resistance Go retains a person’s Bitcoin holdings in self-custody and crypto-native platforms with no custody interval suspension, withdrawal limits, charges, or counterparty threat.

Banks are nonetheless capturing clients who need ETF flows and controlled wrappers. Direct custody of individually held cash is out of attain, and an change constructed for Bitcoin from the start preserves the relationships banks are searching for.

Bitcoin’s institutionalization stage progresses within the order that almost all monetary devices comply with. People first constructed the inspiration of possession years earlier than banks constructed the custodial, lending, and asset administration methods that now compete for a bit of it.

No matter what proportion of that 13.9 million BTC results in bank-managed accounts, the cash already belong to the folks the financial institution is making an attempt to achieve, and possession arrived lengthy earlier than the invites have been despatched.