Metaplanet’s Siiibo contract transforms Bitcoin authorities bond buying and selling from a matter of stability sheet accumulation to a check of regulated distribution.

The Japanese listed firm has agreed to accumulate Siiibo Securities, a regulated company bond platform, giving Japan’s largest Bitcoin-listed treasury agency a path to structuring and distributing securities as mNAV, dilution and BTC per share calculations come beneath stress.

The broader concern has moved from merely copying Treasury’s technique to constructing a licensed channel that may bundle Bitcoin publicity whereas preserving the BTC per share claims that made the commerce engaging within the first place.

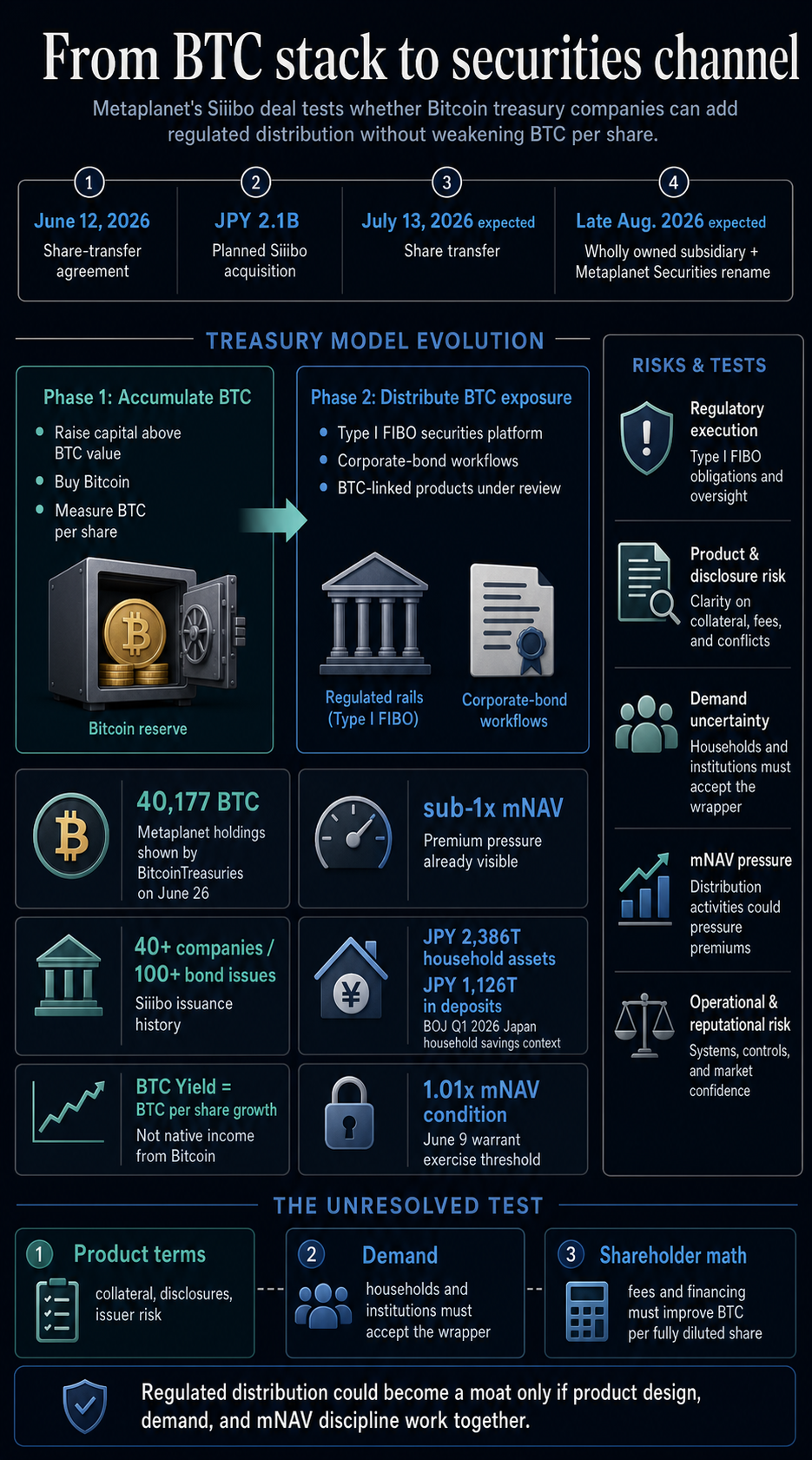

In accordance with Metaplanet’s June 12 disclosure, the corporate has entered right into a inventory switch settlement to accumulate Siiibo for two.1 billion yen, and after finishing the required procedures, the inventory switch is scheduled to happen on July 13, with the corporate scheduled to turn out to be an entirely owned subsidiary in late August.

In accordance with the corporate, Siiibo will probably be renamed Metaplanet Securities after its closure.

Bitcoin Treasuries’ Metaplanet profile seen on June twenty sixth confirmed that the corporate held 40,177 BTC, whereas the underlying and diluted mNAV numbers remained under 1x.

On this context, the Siiibo deal is a check of whether or not treasury firms can construct their companies round Bitcoin publicity, fairly than relying totally on recurring equity-linked loans.

Regulated rails and Bitcoin per share

Siiibo gives Metaplanet with a securities platform with regulatory data and operational historical past. Japan’s Monetary Companies Company lists Siiibo Securities as a monetary devices enterprise operator, and Metaplanet describes the corporate as a registered first-class monetary devices enterprise operator that operates a web-based platform centered on company bonds.

In accordance with Metaplanet paperwork, Siiibo has supported over 100 company bond issuances, underwritings, and solicitations for over 40 firms.

This file has operational worth, as this acquisition gives greater than authorized standing. This allows issuance workflows, compliance processes, issuer relationships, and distribution experiences for buyers.

The corporate’s supplementary supplies clearly point out that route. Metaplanet stated the acquisition is centered round “bringing yield to Japan” and that it intends to discover digital monetary merchandise similar to income-oriented BTC-related merchandise, personal placement bond merchandise, merchandise incorporating Bitcoin-related property, and safety tokens by means of the Siiibo channel.

These are product ideas which can be nonetheless into consideration fairly than launched merchandise, however they signify the strategic form of this motion.

For Bitcoin treasury firms, the distinction is essential. Passive monetary fashions depend on entry to capital and the market’s willingness to worth an organization above BTC.

The brokerage platform creates charges, distributions, product design, and direct entry potentialities for buyers who need Bitcoin-related publicity in a regulated wrapper.

The yield language additionally requires an correct denominator. On its about web page, Metaplanet states that BTC yield is a key efficiency metric, defining it as Bitcoin per share progress.

This metric measures stability sheet progress fairly than revenue paid by Bitcoin itself.

If Metaplanet finally provides a yield-style Bitcoin product, its revenue will have to be derived from a disclosed construction round BTC, similar to credit score spreads, mortgage collateral, choice premiums, issuer threat, tokenized safety preparations, or one other outlined mechanism.

Bitcoin itself doesn’t generate native coupons.

MetaPlanet’s June 9 warrant disclosure reveals why that distinction is central to the mannequin. The corporate has revised the minimal train circumstances for the twenty seventh inventory acquisition rights in order that they will solely be exercised if mNAV is 1.01 instances or extra.

Metaplanet stated this situation is aimed toward avoiding workout routines which can be unlikely to extend the worth of every Bitcoin share and will trigger dilution.

This is similar stress that each one finance firms face when the low premiums put on off. Issuance could improve if the inventory trades at a big premium to BTC worth.

If the premium compresses or disappears, the identical funding instrument may dilute current rights on the Bitcoin stack.

Product companies could add a second engine, however must be judged on the identical denominator: totally diluted BTC per share earlier than charges, debt, first-class claims, and working prices.

Japan’s financial savings market adjustments course

Metaplanet’s technique diverges from the technique’s capital markets mannequin by including a licensed Japanese securities platform and stuck revenue product ambitions.

Whereas the technique stays the reference level for the size model of Bitcoin accumulation by public firms, Metaplanet’s Siiibo transfer is extra home and distribution-driven.

It’s constructed round regulated securities distribution, company bonds, and a financial savings market with an unusually massive money base.

In accordance with the Financial institution of Japan’s Movement of Funds Information Report for the primary quarter of 2026, the monetary property held by households as of the top of March had been 2,386 trillion yen, of which 1,126 trillion yen was held in foreign money and deposits.

This massive variety of deposits explains why firms are in search of regulatory compliance for Bitcoin-related merchandise denominated in yen or distributed in Japan.

A big financial savings pool signifies a prepared market fairly than a confirmed demand.

The ultimate product phrases will decide whether or not the proposal is extra of an issuer threat product with straight publicity, structured credit score, leveraged yield, tokenized claims, or Bitcoin branding.

That is the place Treasury transactions turn out to be extra complicated. Publicly traded firms can maintain Bitcoin in a method that’s traceable to their shareholders.

Whereas regulated product platforms could increase entry and doubtlessly generate payment revenue, additionally they introduce product-level dangers, disclosure obligations, questions relating to suitability for distribution, and potential liabilities separate from the BTC reserves themselves.

The broader Bitcoin treasury sector of public firms has additionally grown massive sufficient for these inquiries to turn out to be essential throughout a number of issuers.

BitcoinTreasuries tracks roughly 199 public firms holding roughly 1.264 million BTC, and capital construction and valuation self-discipline is just not a single firm concern.

With current stories on the treasury firm’s shareholder value and Strategic’s financing pivot, the dialogue has already moved past the headline accumulation to questions of financing phrases, dilution, senior debt, and whether or not totally diluted BTC per share will truly enhance.

The acquisition of Metaplanet is a brand new model of the identical argument. If a treasury firm wants Bitcoin-related enterprise operations, the standard of these companies will probably be as essential as the scale of the Bitcoin pile.

Product design shapes outcomes

Metaplanet’s Siiibo transfer suggests the Bitcoin treasury firm is testing the transition from an accumulation car to a monetary merchandise firm.

That benefit will come from licensing, distribution, belief, writer relationships, product design, in addition to having BTC on public stability sheets early on.

This may very well be a constructive for Metaplanet if the corporate makes use of Siiibo to construct a clear, inexpensive product that generates income whereas supporting a BTC per share technique.

Moreover, new dangers may come up if the yield language attracts buyers into buildings the place returns rely upon leverage, credit score publicity, collateral circumstances, or issuer obligations which can be extra obscure than spot publicity to Bitcoin.

The following verify is restricted. The deliberate inventory switch date of July thirteenth and the conversion right into a subsidiary in late August will decide whether or not the platform acquisition will probably be accomplished as deliberate.

Product filings, time period sheets, collateral guidelines, threat disclosures, distribution limits, and buyer demand will point out whether or not Metaplanet Securities will turn out to be an actual working engine.

For the broader finance sector, the teachings are larger than one Japanese deal.

If mNAV premiums are excessive, the mannequin seems easy. Simply concern shares, purchase Bitcoin, and repeat. As premiums compress, companies want stronger solutions.

Metaplanet seeks to offer a solution by means of licensing distribution and yield-style product design.

The result will rely upon whether or not these regulated channels truly enhance the economics of possession for shareholders.

Securities distributions may very well be the following moat for Bitcoin treasury firms if they will generate lasting charges, disciplined product demand, and elevated BTC per share.

If complexity will increase round unstable reserve property, markets could deal with the transfer as one other type of leverage with a regulatory guise.