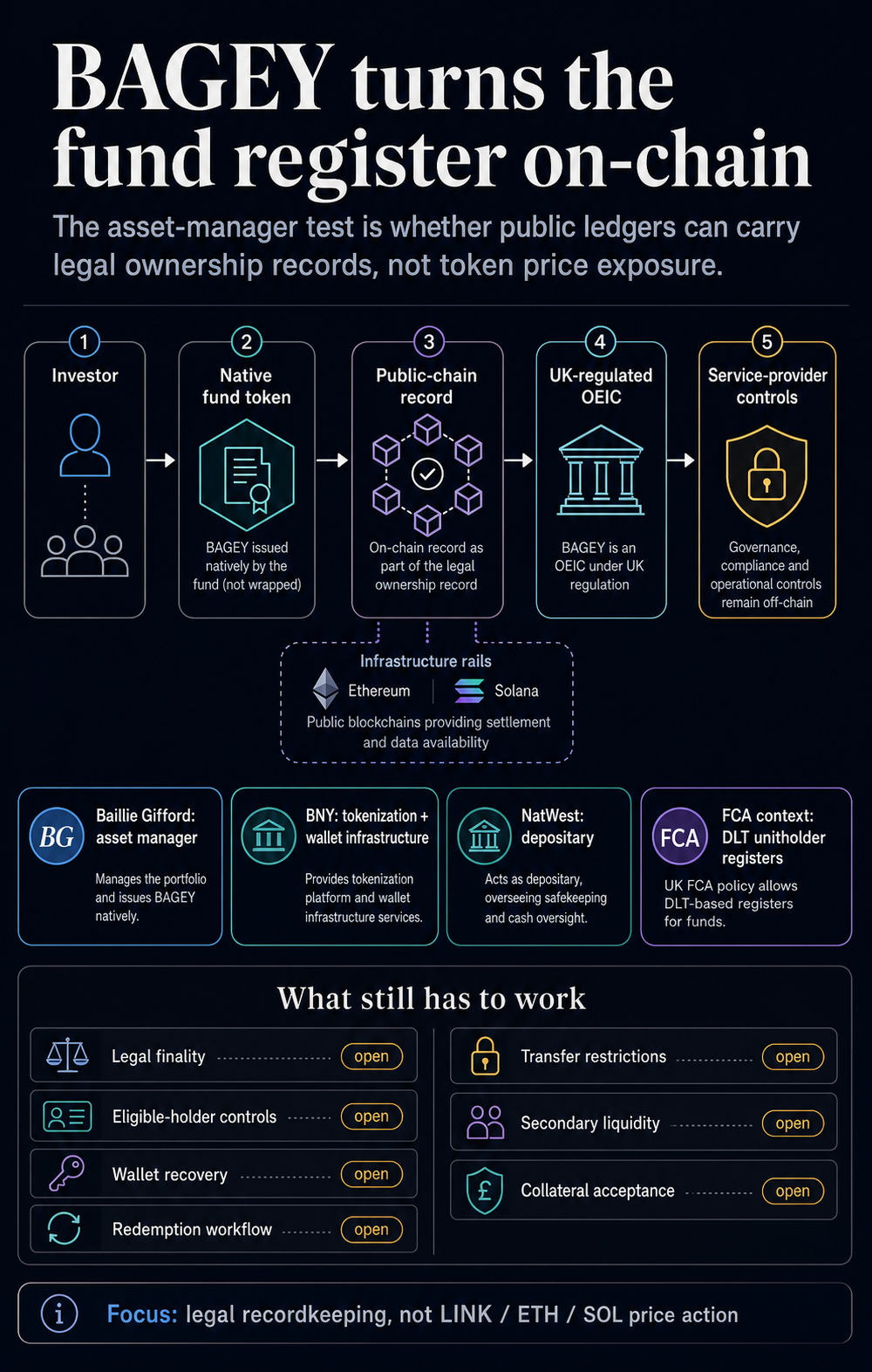

The British funding supervisor, which has greater than £286 billion ($377 billion) in property underneath administration, is utilizing BAGEY to check a sharper model of fund tokenization. Public blockchains are used as a part of the file of possession for regulated UK funds.

This may finally transfer the dialogue of tokenization to fund administration relatively than simply distribution. A tokenized fund could possibly be a blockchain-style declare on a conventional product the place the definitive possession file resides elsewhere.

Baillie Gifford presents a extra strong mannequin by which on-chain information kind a part of the authorized title register itself.

In that model, the token turns into a way of recording buyers’ holdings. The outcomes are seen. If regulated fund possession can survive natively on the general public chain, the change is within the fund administration stack, not the crypto market publicity.

Baillie Gifford’s digital asset documentation frames tokenization as an improve to possession information, funds, entry, and consumer outcomes. What’s fascinating is that information and processes can behave in a different way when possession is expressed on shared rails.

This announcement solutions one slim query concerning tokenized funds with a certified “sure.” Regulated funds are transferring to authorized infrastructure on the general public chain relatively than blockchain-wrapped variations of present merchandise.

This mannequin nonetheless must show that it could possibly assist secondary transfers, 24-hour settlement, or using collateral exterior of a managed major market setting.

Native issuance strikes possession information via tokenization

The central declare about BAGEY is native publication. Baillie Gifford described the fund as a completely native UK-regulated tokenized fund working via a UK-regulated OEIC construction, issuing on Ethereum and Solana, with BNY offering the tokenization and pockets infrastructure and NatWest Trustee and Depositary Companies appearing as depositary.

If a blockchain is a authorized registry, fund managers, custodians, switch brokers, depositaries, and buyers are aligned round greater than only a non-public database that later matches their tokens.

A shared ledger turns into a part of the file of who owns what.

That is very completely different from tokenized wrappers. The wrapper permits buyers to offer blockchain-based entry to fund exposures whereas protecting a legally definitive register inside conventional infrastructure.

That is nonetheless helpful, however the middle of gravity of the conduct stays off-chain. BAGEY’s extra vital argument is that the vinyl layer itself has moved.

| mannequin | The place possession exists | Function of token | Principal query |

|---|---|---|---|

| Native tokenized fund | On-chain information are offered as a part of the fund possession register. | Information an investor’s direct holdings in a regulated fund. | Can authorized, custody, switch, and assortment controls be maintained in a manufacturing surroundings? |

| tokenized wrapper | Information of one other fund or administrator stay the definitive supply | Represents entry to off-chain merchandise | Does the wrapper add any actual utility past distribution? |

| crypto publicity merchandise | Conventional product information stay central | Gives publicity to tokens, chains, or associated methods | How do asset costs change? |

This distinction makes LINK, ETH, and SOL value fluctuations secondary. Whereas Chainlink expands its launch and Ethereum and Solana present public chain infrastructure, the information facilities on whether or not fund possession might be natively recorded on a shared public ledger inside a regulated construction.

UK context turns tokenization into fund plumbing

Primarily British background. The Monetary Conduct Authority revealed PS26/7 on Fund Tokenization on 30 April, setting out how licensed fund managers can use distributed ledger know-how inside their present licensed fund framework.

This coverage assertion covers tokenized fund fashions and DLT-based unitholder registries, offering BAGEY with a regulatory framework past a standalone product launch.

bookmydollar beforehand coated the UK’s transfer to approve the tokenization of FCA-approved funding funds. This early shift is critical as BAGEY is now supporting coverage route with the implementation of particular asset managers, fund buildings, service supplier stacks, and public chains.

It additionally follows tokenized fund experiments with Chainlink, Swift, UBS and others testing automation of subscriptions and redemptions and switch brokers. These pilots demonstrated that conventional treasury workflows might be built-in with blockchain programs.

BAGEY deepens his doubts. The related query is just not whether or not a single workflow might be automated, however whether or not a regulated fund possession file can reside natively in public chain infrastructure.

For asset administration firms, the burden of proof will change. Tokenized fund wrappers might be evaluated primarily based on entry, distribution, and investor demand.

Native fund information have to be assessed for authorized finality, operational resilience, management of eligible holders, failed or misdirected transfers, misplaced wallets, sanctions evaluation, timing of redemptions, and when blockchain entries change into enforceable in opposition to the fund.

These are sensible back-office particulars. These decide whether or not the token is helpful past issuance and redemption.

Fund tokens that may be trusted as authorized possession information may theoretically be extra simply moved between licensed holders and settled exterior of conventional market hours, as counterparties can confirm and belief the possession information. If these authorized and operational controls stay restricted, tokenization will transfer nearer to a managed distribution channel.

Comparable precautions apply to collateral. Whereas Baillie Gifford’s intensive tokenization documentation discusses asset mobility and buyer outcomes, BAGEY’s launch file alone doesn’t show that fund tokens are already accepted as collateral throughout market venues.

That is why the next disclosures are simply as vital as the discharge label. It’ll present whether or not on-chain registers will change the day-to-day operation of funds, or whether or not they are going to primarily change the best way merchandise are issued.

The subsequent check is to verify operation

BAGEY reveals that enormous conventional asset managers are eager to place their regulated fund buildings on the rails of public chains, explaining that the result’s native relatively than wrapped. It additionally signifies that enormous service suppliers could also be included into the construction.

BNY’s infrastructure position and NatWest’s depository position are vital as a result of regulated funds don’t change into authorized infrastructure solely via good contracts. They want oversight, settlement, administration, custody procedures, and investor safety that establishments can uphold.

This announcement stops in need of indicating that tokenized fund models will probably be freely traded across the clock, extensively accepted as collateral, or substitute the remainder of the fund administration stack. These outcomes require proof of precise switch mechanisms, secondary liquidity, investor onboarding, redemption historical past, and authorized remedy underneath stress.

That would be the subsequent check for tokenized funds. The business already is aware of that monetary merchandise might be represented on blockchain.

A harder query is whether or not regulated entities deal with public chain information as locations the place authorized possession is established, up to date, and trusted by different market individuals.

When the reply is sure, tokenization is now not primarily about packaging. It might be a change within the plumbing behind fund possession.

Asset managers will then compete not solely on product publicity, but in addition on the velocity, transparency, portability and operational reliability of fund information.

If the reply stays partial, BAGEY should still be vital, however its that means is extra restricted. This may display that native issuance can operate inside a managed surroundings whereas abandoning an important market features resembling peer-to-peer transfers and using collateral.

For now, BAGEY strikes the dialogue ahead with out ending it. This isn’t proof that public blockchains have already changed the outdated cash administration stack, however relatively a stay check of whether or not public blockchains can keep regulated possession information.