The roughly $150 million prediction market was thrown into turmoil after platform Polymarket moved to refuse to pay a dealer who accurately predicted that company finance agency Technique would promote a few of its Bitcoin holdings.

The controversy focuses on a elementary disconnect between when an occasion happens and when it’s made public, exposing structural flaws in the best way decentralized prediction markets settle billions of {dollars} of bets. Bettors are presently embroiled in a bitter dispute over a technical difficulty that might wipe out tens of millions of {dollars} in payouts that merchants believed had been assured.

On June 1, Technique, a enterprise intelligence agency (previously MicroStrategy) with roughly $60 billion in high crypto belongings, filed regulatory paperwork confirming that it bought 32 Bitcoins value roughly $2.5 million between Could 26 and Could 31.

For members in a polymarket contract asking if Technique would promote their Bitcoin by Could thirty first, the 8-Okay submitting gave the impression to be conclusive proof of a “sure” consequence.

Nevertheless, the market is presently transferring by way of a contentious decision course of that strongly favors a “no.”

Polymarket directors issued a press release after the deadline stating that the transaction didn’t fall throughout the platform’s working practices as there was no public affirmation of the sale till June 1.

The scenario has raised widespread suspicions of market manipulation and has drawn intense scrutiny to decentralized betting mechanisms at a time when prediction platforms are looking for legitimacy in mainstream finance.

Timeline of disputed polymarket transactions

The continued dispute stems from particular language within the contract that states that if Technique sells its Bitcoin by 11:59pm ET on Could thirty first, the market will vote sure.

This rule explicitly designated an organization’s public data and on-chain knowledge as the first supply of decision.

When Technique filed its necessary 8-Okay disclosure on June 1, the market was nonetheless open for energetic buying and selling. A number of merchants, who noticed that the corporate objectively executed gross sales forward of the Could 31 deadline, rushed to reap the benefits of what they perceived to be pricing inefficiencies.

One market participant, going by the pseudonym willo2, wager $527,000 on “Sure” after studying the regulatory submitting. Even after the disclosure, merchants anticipated a 20% arbitrage alternative, because the market had priced within the odds of a sale at round 80 cents on the greenback.

As an alternative, the dealer misplaced his complete $500,000 principal. Following the inflow of capital, Polymarket added clarification to its market description, stating that confirmations exterior the required interval won’t be accepted.

Relating to these occasions, Willo writes of X:

“This was not a part of the foundations in any respect. It was not written into the market and it made no sense. And above all, Polymarket itself didn’t imagine in it. Why? As a result of if that had been true, the market ought to have closed on Could thirty first. The market didn’t shut.”

Market analysts have extensively condemned the flip of occasions. Jeff Dorman, chief funding officer at digital asset administration agency Arca, pointed to a serious logical inconsistency within the platform’s dealing with of timelines.

Dorman identified that if the contract’s strict phrases dictated that it finish precisely at midnight on Could thirty first, the platform ought to have stopped all buying and selling at that precise second.

He mentioned permitting members to proceed shopping for shares on June 1 whereas making use of the Could 31 affirmation deadline retroactively created a entice for merchants counting on conventional authorized interpretations of contract language.

Jonathan Paresen, a knowledge scientist who screens decentralized platforms, characterised the platform’s habits as a type of fraud by omission.

Pallesen argued that whereas requiring affirmation of stories to coincide with occasion deadlines is an affordable precaution in opposition to indefinite market delays, the failure to explicitly codify the apply into contract guidelines exploits particular person bettors.

Institutional merchants who had been acquainted with the platform’s unstated conventions had been in a position to extract massive sums of cash from customers who moderately assumed {that a} accomplished sale meant a successful ticket.

UMA oracle vulnerability

The strategic debate escalated from a single contract to a referendum on the funds structure underlying the polymarket.

In contrast to conventional monetary exchanges, which depend on centralized clearinghouses or compliance departments to clear derivatives, Polymarket outsources truth-checking to Common Market Entry (UMA).

UMA acts as an “optimistic oracle,” a decentralized community through which token holders vote to resolve disputed outcomes.

Beneath this framework, any consumer can contest a proposed market settlement by staking a $750 bond. If the result’s contested a number of instances, the choice will default to a vote by UMA cryptocurrency holders.

The ultimate fee is set by the burden of the tokens solid, quite than by an goal judicial evaluate of the details.

Critics argue that the system is very weak to manipulation. Eric Connor, a outstanding cryptocurrency analyst, identified that the token voting mannequin is structurally compromised.

Connor argued that giant token holders, sometimes called whales, can use ambiguous contract guidelines as a weapon to guard their monetary place and keep away from large losses by ignoring goal actuality.

Current knowledge helps these issues. A WSJ investigation into the platform’s voting mechanism revealed that the ten largest wallets account for greater than half of the votes in most disputes on Polymarket.

Moreover, roughly 60% of energetic UMA voters had been straight related to Polymarket’s stay accounts, and one in 5 contested markets had voters with a direct monetary stake within the consequence of the arbitration.

Polymarket has already recorded greater than 1,150 disputed markets within the first 5 months of 2026, greater than the earlier yr’s complete.

The platform itself has restricted recourse, as its decentralized construction technically doesn’t permit inner directors to override the ultimate UMA token vote.

Mainstream development encounters decentralized friction

The timing of the $150 million dispute is precarious for the prediction markets sector, which has aggressively expanded into conventional finance and media over the previous few years.

Throughout this era, platforms Polymarket and Kalshi have actively distanced themselves from being labeled as unregulated crypto casinos.

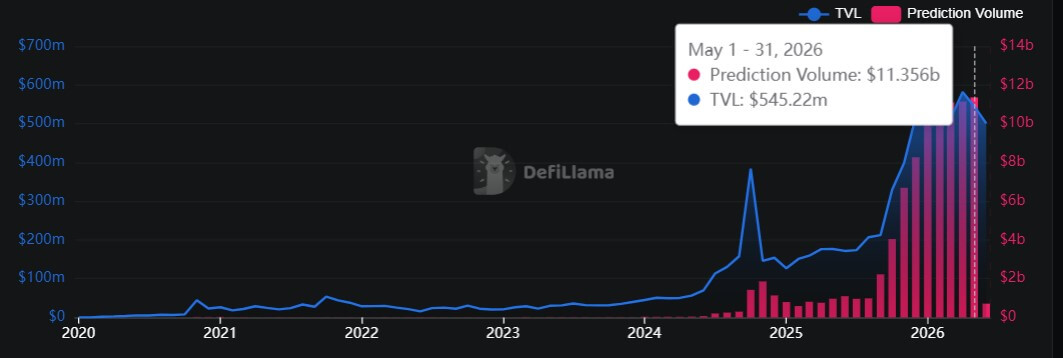

Nevertheless, buying and selling quantity elevated quickly and exceeded $10 billion in Could 2026. In keeping with DeFiLlama knowledge, this marks a 10x enhance in comparison with the identical interval final yr.

On the similar time, it has signed content material and knowledge integration agreements with main establishments such because the New York Inventory Change, Dow Jones, Related Press, and Fox Information.

This speedy institutionalization follows years of intense regulatory friction. In 2022, the Commodity Futures Buying and selling Fee (CFTC) pressured Polymarket to shut its U.S. operations and relocate abroad.

Mr. Kalsi then engaged in a prolonged authorized battle with the CFTC over his proper to host political occasion contracts, finally successful in a landmark federal courtroom case in late 2024.

However the regulatory setting modified after the 2024 presidential election, when the platforms accurately predicted Donald Trump’s victory.

Since then, the platform has acquired vital regulatory assist, with Polymarket buying a federally chartered derivatives alternate and the CFTC additionally asserting unique rights to control these markets.

CFTC Chairman Michael S. Selig mentioned:

“Occasion contracts permit companies and people to hedge event-driven dangers, permit traders to handle portfolio exposures, and supply data to the general public concerning the end result of future occasions. These merchandise are commodity derivatives and are exactly throughout the CFTC’s regulatory authority.”

Regardless of securing a regulatory foothold, the fundamental mechanics of decentralized prediction markets stay extremely experimental.

In conventional inventory markets, deep liquidity and strict regulatory oversight usually be certain that asset costs mirror substantive actuality.

On platforms managed by tokenized voting programs, the definition of actuality continues to be up for debate.

Till these structural dispute mechanisms mature, merchants navigating the burgeoning prediction market economic system will stay on the mercy of unwritten guidelines and decentralized juries.